QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

Hello大家好,我是高頓財經(jīng)研究院的Phoebe老師。由于很多同學(xué)反映在考試中,做到合并報表大題的時候時間已經(jīng)所剩不多,而且對整個大題也不知道如何下手。今天Phoebe老師來給大家整理一下FA中必考題型之合并報表的幾大常見考點,以幫助更多同學(xué)在該題型的考察中更快更精準地得到大部分的分數(shù)。

①判斷控制成立的條件:

An investor controls an investee if and only if the investor has all the following(形成控制同時需要滿足以下三大條件):

A)Power over the investee to direct the relevant activities;

B)Exposure,or rights,to variable returns from its involvement with the investee;

C)Ability to use its power over the investee to affect the amount of the investor’s returns.

Example of control(常見的例子有):

A)Voting rights(>50%ordinary shares);

B)Rights to appoints,reassign or remove key management personnel;

C)Rights to appoint or remove another entity that directs relevant activities;

D)Management contract.

②購買對價consideration計算:

Consideration may consist of(常見的對價有cash和shares兩種)

A)Cash(以cash的形式進行收購,直接記錄cash值)

P purchased xx shares/xx%of shares of S for XX

P purchased xx shares/xx%of shares of S for XX per share

B)Shares(以股換股)

Share exchange on a X for Y basis(代表每獲取子公司Y股股票,母公司需付出X股股票)

Share consideration=母公司獲取子公司股數(shù)*X/Y*母公司收購日股價

③商譽的計算:

Goodwills=Considerations+NCI at acquisition date-FV of net assets of S at acquisition date

計算Goodwill的時候,用的是consideration的公允價值,加上NCI的公允價值,減去子公司的凈資產(chǎn)(net assets)。其中的retained earning和share capital,是用子公司在收購日當天的數(shù)字。

④未實現(xiàn)利潤PUP(provision for unrealised profit)的計算:

首先根據(jù)內(nèi)部銷售的售價和成本把利潤算出來,再考慮期末還沒賣出去的(還留在庫存里的部分)對應(yīng)的比例,計算出這部分unrealised profit的值。

未實現(xiàn)利潤PUP(provision for unrealised profit)的影響:

A)P sold to S:

Group RE=母公司RE-URP+子公司收購后產(chǎn)生的RE*P%

NCI at reporting date=NCI at acq.date+子公司收購后產(chǎn)生的RE*NCI%

B)S sold to P:

Group RE=母公司RE+(子公司收購后產(chǎn)生的RE-URP)*P%

NCI at reporting date=NCI at acq.date+(子公司收購后產(chǎn)生的RE-URP)*NCI%

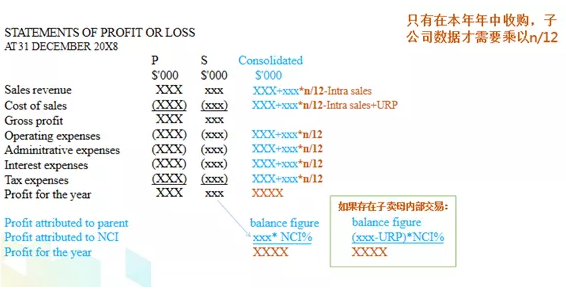

⑤合并利潤表:

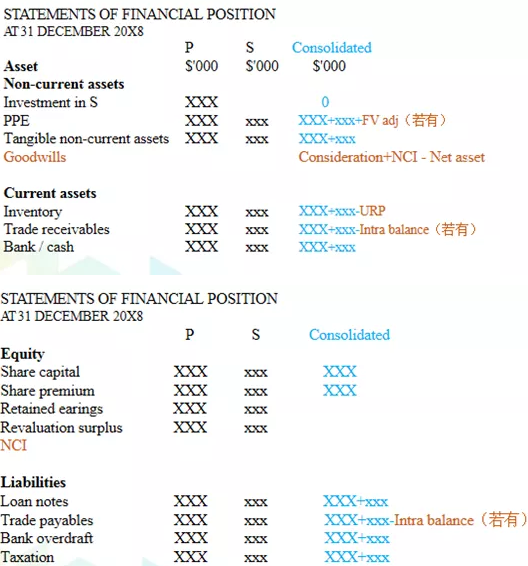

⑥合并資產(chǎn)負債表:

A)Share capital/share premium是母公司單體報表里的數(shù)值。

B)Retained earnings=Parent's retained earnings+Group's share of post reatained earnings-unrealised profit。

C)NCI=fair value at acquisition+share of post-acquisiton retained earnings。另外,如果是子公司賣貨給母公司,則要另外考慮PUP屬于少數(shù)股東的份額。

本文來源:ACCA學(xué)習(xí)幫,轉(zhuǎn)載請后臺留言聯(lián)系授權(quán),侵權(quán)必究。