QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

財(cái)務(wù)報(bào)告與分析中章節(jié)的設(shè)置是循序漸進(jìn)、逐層深入的,前面介紹的術(shù)語在后面還會(huì)有詳細(xì)的解釋與探討。

由于財(cái)務(wù)報(bào)告與分析本身自立體系,它是上市公司和報(bào)表使用人之間溝通交流的語言,所以學(xué)起來與外語學(xué)習(xí)有幾分相似。

財(cái)務(wù)報(bào)告與分析一共分為四大部分:

第一部分是掃盲階段,主要介紹財(cái)務(wù)術(shù)語、體系等基本知識(shí)。

在此基礎(chǔ)上,第二部分更深入地講解財(cái)務(wù)報(bào)表編制以及財(cái)務(wù)報(bào)表分析的方法。

進(jìn)一步地,第三部分針對(duì)存在利潤操縱空間的重點(diǎn)科目做詳細(xì)、深入的討論。

最后,第四部分是前面三部分內(nèi)容的綜合應(yīng)用。

四大部分在考試中占比最大的是第二部分和第三部分,大概占財(cái)報(bào)分析所有題目的80%以上。其次是第一部分,占比10%左右。

由于第四部分是財(cái)務(wù)分析的綜合應(yīng)用,不太適合一級(jí)的出題形式,所以出題比例相對(duì)比較少,大概占5%左右。

"Financial Report":Long-Lived Assets

Questions 1:

If an analyst is concerned about the liquidity of a company’s inventory,he would most likely look in the notes to the financial statements to determine the:

A、amount of inventories recognized as expense during the period.

B、cost formula or inventory valuation method used.

C、breakdown of inventory between work in progress and finished goods.

【Answer to question 1】C

【analysis】

C is correct.The breakdown between work in progress and finished goods provides liquidity information because finished goods are ready to ship and thus more liquid than work in progress.

A is incorrect.The amount of inventories expensed as cost of goods sold has no effect on the liquidity of the inventory on hand.

B is incorrect.The inventory valuation method used is unrelated to the liquidity of the inventory.

Questions 2:

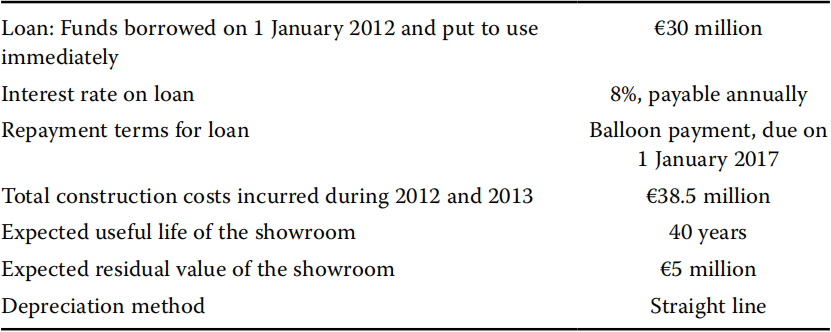

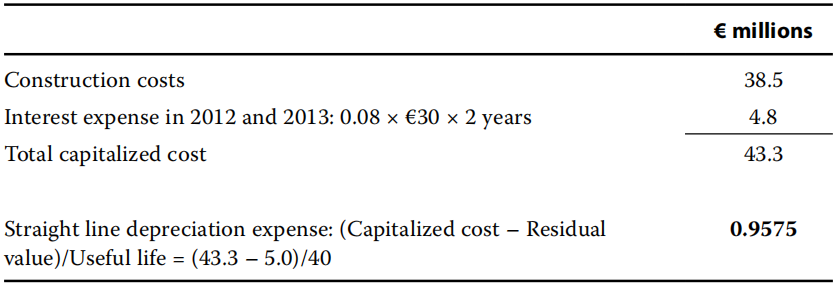

The following information is available concerning a new showroom a company built.Construction started on 1 January 2012,and the grand opening was on 1 January 2014:

The depreciation expense(in millions)for the showroom in 2014 is closest to:

A、€1.0175.

B、€0.9575.

C、€0.8375.

【Answer to question 2】B

【analysis】

B is correct.Because the asset is self-constructed,the costs of specifically identifiable interest during the construction period can be capitalized and included in the cost of the showroom.

A is incorrect.It continues to capitalize the interest in 2014:(43.3+2.4–5.0)/40=1.0175.

C is incorrect.It does not include the capitalized interest:(38.5–5)/40=0.8375.

相關(guān)閱讀

延伸閱讀

以上就是【CFA財(cái)務(wù)報(bào)表分析練習(xí)題之長期資產(chǎn)】的全部內(nèi)容,如果你想學(xué)習(xí)更多CFA相關(guān)知識(shí),歡迎大家前往高頓教育官網(wǎng)CFA頻道!在這里,你可以學(xué)習(xí)更多精品課程,練習(xí)更多重點(diǎn)試題,了解更多最新考試動(dòng)態(tài)。