QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

大家好,今天我們來(lái)看下Non current assets held for sale有關(guān)的知識(shí)點(diǎn)。

1

對(duì)于Non current assets held for sale,它和Non current assets以及Current assets是不一樣的。

比如說(shuō)Non current assets中的PPE,它持有的目的就是作為企業(yè)的固定資產(chǎn),長(zhǎng)期持有的。再比如說(shuō)Current assets中的inventory,一開(kāi)始的目的就是為了交易而產(chǎn)生的。對(duì)于Non current assets held for sale它本身是可以使用很多年的,但是現(xiàn)在持有的時(shí)間不足一年了。

所以我們對(duì)于Non current assets held for sales是要單獨(dú)列示在資產(chǎn)負(fù)債表中的。

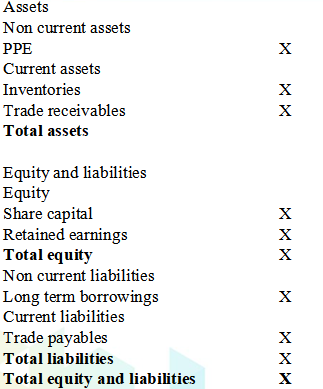

通常我們所看到的資產(chǎn)負(fù)債表是這樣的:

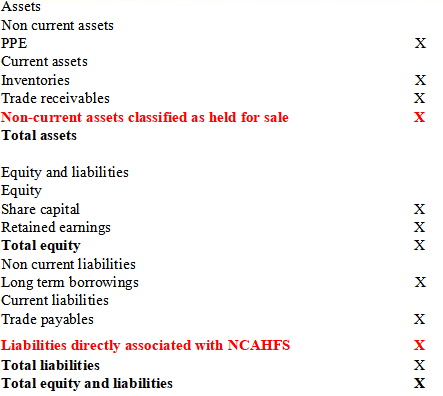

但是有了Non current assets held for sale之后,我們的報(bào)表就要變成這樣:

所以大家在這里要知道的是Non current assets held for sale是需要單獨(dú)列示在資產(chǎn)負(fù)債表中。

2

那么什么時(shí)候可以劃分為Non current assets held for sale呢?它必須滿足:

1.對(duì)于Non current assets held for sale,它必須是一個(gè)銷售的交易,而不是持續(xù)的使用。

2.The asset must be available for immediate sale in its present condition.在當(dāng)前可達(dá)到立即出售的條件。

3.Its sale must be highly probable.銷售是非常有可能的。

那什么情況下,意味著是Its sale must be highly probable呢?

1.Management must be committed to a plan to sell the asset.管理層承諾有計(jì)劃去賣。

2.There must be an active programme to locate a buyer.已經(jīng)開(kāi)展活動(dòng),很積極的去尋找買(mǎi)家。

3.The asset must be marketed for sale at a price that is reasonable in relation to its current fair value.資產(chǎn)的售價(jià)相對(duì)來(lái)說(shuō)是合理的。

4.The sale should be expected to take place within one year from the date of classification.從劃分日開(kāi)始,銷售會(huì)在一年內(nèi)完成。

5.It is likely that significant changes to the plan will be made or that the plan will be withdrawn.該計(jì)劃,基本上不能取消。

這就是highly probable的條件。

在這里,是有2個(gè)特殊的情況的:

第一種情況,如果因?yàn)椴豢煽氐囊蛩兀瑢?dǎo)致已經(jīng)劃分為NCA held for sale的資產(chǎn),沒(méi)有辦法在一年內(nèi)出售的,比如說(shuō)政府出臺(tái)了政策,導(dǎo)致沒(méi)有辦法再一年內(nèi)出售了,這個(gè)時(shí)候,仍然是可以劃分為NCA held for sale的。除此情況導(dǎo)致的沒(méi)有辦法在一年內(nèi)賣出的,就要停止劃分為NCA held for sale。

第二種情況,購(gòu)買(mǎi)這個(gè)子公司的目的,一開(kāi)始就是為了漲價(jià)之后再賣出的,那么如果想要在最開(kāi)始就劃分為持有待售,就必須要滿足:1-一年內(nèi)賣出;2-Highly probable的條件要在三個(gè)月之內(nèi)完成。

3

那么接下來(lái),我們?cè)賮?lái)看下與Non current assets held for sale計(jì)量有關(guān)的知識(shí)。

大家在這里要注意的是,Non current assets held for sale無(wú)折舊,無(wú)增值,只減值。

比如說(shuō)固定資產(chǎn)在2019年6月30日的賬面價(jià)值是50W,且在這一天的時(shí)候,劃分成為了Non current asset held for sale。那么這個(gè)時(shí)候,我們要做的會(huì)計(jì)分錄就是:

Dr NCAHFS 50W

Cr PPE 50W

并且在轉(zhuǎn)為NCAHFS之后,就不能再計(jì)提折舊了。

而且NCAHFS它的減值是與眾不同的,它是按照carrying amount與fair value less cost of disposal孰低來(lái)進(jìn)行計(jì)量的。比如說(shuō)減值之后的金額是47,那么這個(gè)時(shí)候,要做的會(huì)計(jì)分錄就是Dr P&L 3 Cr NACHFS 3W,它的減值是要進(jìn)入到利潤(rùn)表的。

知識(shí)點(diǎn)說(shuō)完了,下周我們繼續(xù)講解關(guān)于Non current assets held for sale的相關(guān)題目~